Everyone loves a winner. And for the past few years, a handful of mega cap technology companies have been the only winners that mattered on Wall Street.

That story is starting to change.

I spend my days analyzing equity and fixed income markets from Darien, Connecticut. What I am watching closely right now is a shift that does not make many headlines. It is quiet, it is data driven, and it could be one of the most important investing opportunities in years.

It comes down to this. The market is broadening.

The Big Get Bigger, Until They Don’t

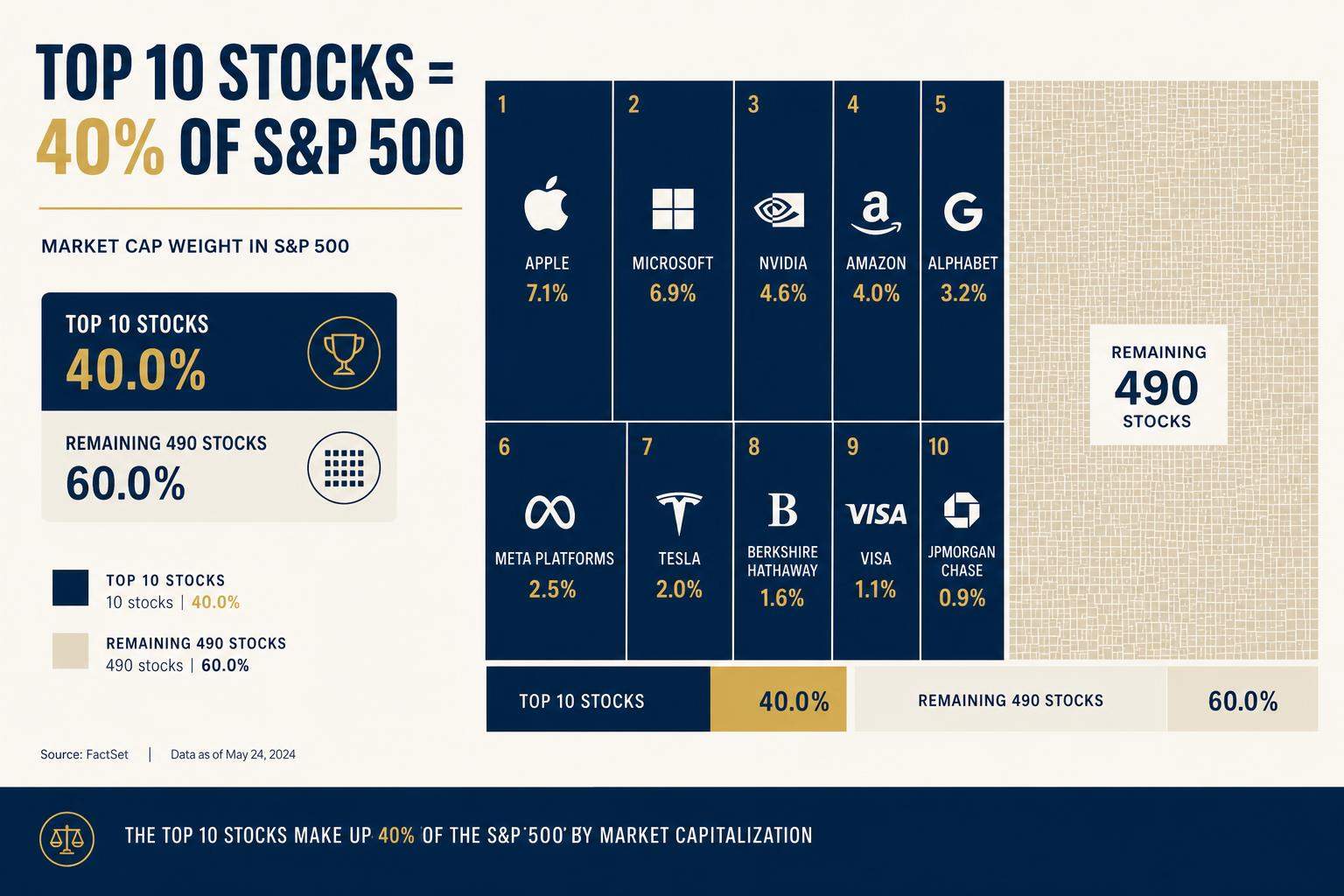

The S&P 500 has delivered strong returns. No one disputes that. But concentration has reached a level that should make thoughtful investors pause. According to market research cited across 2026 outlooks, the top 10 stocks in the S&P 500 now account for more than 40 percent of the index. That is remarkable. It also creates a fragile setup.

When a small number of companies drive a large share of returns, diversification gets harder. It also means the rest of the market gets overlooked. That is where things start to get interesting for patient investors who are willing to do the work.

Goldman Sachs has forecast that the S&P 500 could rise to 7,600 by year end 2026, which implies further upside for the index. That is a constructive outlook. But the more compelling opportunity may not be inside the same crowded group of names that dominated the last cycle.

That is a big part of how I think about markets today. Leadership can stay narrow for a while. Then, almost quietly, it begins to widen.

The Small Cap Discount Is Hard to Ignore

One of the clearest places to see that widening is in small caps.

Smaller companies have lagged large caps for years. That underperformance has left them trading at a meaningful discount to the broader market. For investors who care about valuation, that matters. A lot.

Historically, smaller companies often traded at a premium because investors were willing to pay more for faster growth potential. Today, that relationship looks very different. Small caps remain discounted relative to the broader market, even as the case for broader earnings participation gets stronger.

I do not think history repeats in a clean line. But I do think valuation gaps like this deserve attention. They often tell you where expectations are too low.

That kind of research driven thinking shapes the way I approach markets and investing more broadly. Readers who want more on my background can visit my biography page or learn more through this portfolio profile.

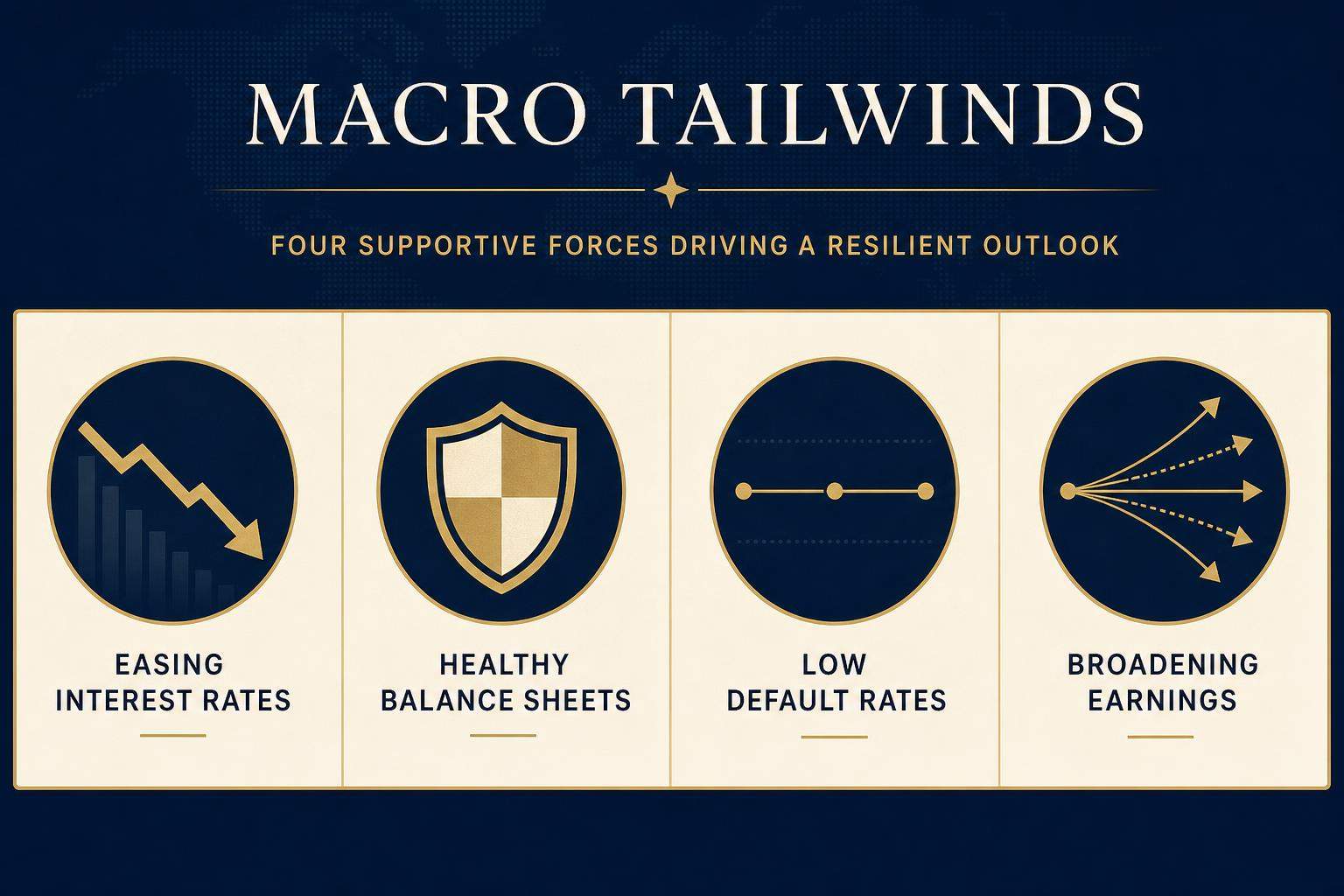

The Macro Setup Looks More Supportive Than Many Realize

From where I sit, the macro backdrop is more supportive for a broader market than many people realize.

AllianceBernstein, Oppenheimer, and other 2026 outlooks have all pointed to a similar theme. Equity leadership is widening. Earnings growth is broadening. And a less fragile market structure may emerge if performance begins to spread beyond the biggest technology platforms.

That shift matters for smaller companies in particular. Lower rates help businesses that rely more heavily on financing. Easier financial conditions, tight credit spreads, and stable balance sheets all support smaller firms more than they support companies already flush with scale and capital access.

That does not mean risk disappears. It never does. Morgan Stanley has been clear that optimism in 2026 still comes with policy risk, political risk, and the possibility of disappointment if market expectations run too far ahead of reality. I agree with that caution. A broadening market is not the same thing as an easy one.

Still, I find the current setup encouraging. Cheap relative valuations, healthier financing conditions, and broader earnings participation are a powerful combination when they show up together.

It is one reason I keep returning to long term thinking. That mindset also shapes my work beyond pure market analysis, including my writing on larger structural themes like navigating the energy transition.

Earnings Are Finally Broadening Beyond Tech

This may be the most important point of all.

For the past several years, investors could tell themselves that nearly all meaningful earnings growth lived inside the same small cluster of giant tech names. In 2026, that story looks less complete.

Analysts now expect stronger earnings participation across a wider set of sectors. Healthcare, industrials, financials, and other areas of the market are showing improving momentum. That reduces dependence on any single sector. It also gives investors more places to find value and more ways to build balanced exposure.

I find that healthy. Markets work better when returns are not carried by the same narrow group of companies year after year.

Goldman Sachs has also noted that AI adoption, fiscal policy shifts, and increased merger activity could create more opportunities for stock pickers in 2026. That is exactly the kind of environment where disciplined research starts to matter more than headline chasing.

What This Means for Fixed Income

On the bond side, the picture is more nuanced.

Yields are still more attractive than they were for much of the past decade. That alone should make fixed income worth revisiting for investors who tuned it out during the low rate years.

Morgan Stanley has suggested favoring equities over credit and government bonds in 2026, especially in the United States. That is a fair view. But it does not mean fixed income has no role. It means being selective.

Short and medium duration investment grade bonds can still provide stability and income. For balanced portfolios, that matters. The goal is not to avoid fixed income. The goal is to use it wisely.

A Darien Perspective on Long Term Discipline

Living and working in Fairfield County, I spend time with people who think carefully about capital. Many of them built wealth not by chasing what was hottest, but by staying patient when others became complacent.

That mindset applies directly to what I see in markets right now.

The AI trade brought enormous attention and enormous capital into a narrow part of the market. It may continue to produce winners. But putting too much into the same crowded names carries real risk. Concentration is not just a statistic. It is a portfolio reality.

Diversification is not a defensive habit. It is a smart one.

If you want to learn more about how I think about markets, research, and long term investing, you can visit davidrewcastle.net or explore additional background at davidrewcastle.com. I also share ideas and visual market inspiration on Pinterest.

The Bottom Line

The bull market may not be over. But leadership is shifting.

The companies that drove returns over the past three years may not be the same companies that drive the next three. The opportunity I see is in quality businesses trading at discounts, earnings growth broadening beyond technology, and balanced portfolios that treat fixed income as a useful tool rather than an afterthought.

That is where value gets created. That is where I focus my work.

David Rewcastle is an Equity and Fixed Income Analyst based in Darien, Connecticut. This article is for informational purposes only and does not constitute investment advice. Always consult a qualified financial professional before making investment decisions.

David Rewcastle of Darien, Connecticut, is an Equity and Fixed Income Analyst with a background in Finance and Middle East Studies